Developing a Model for Audit Documentation Quality Using Internet-Based Technologies Based on a Grounded Theory Approach

Keywords:

Audit documentation, Internet-based technologies, big data, information technology, audit qualityAbstract

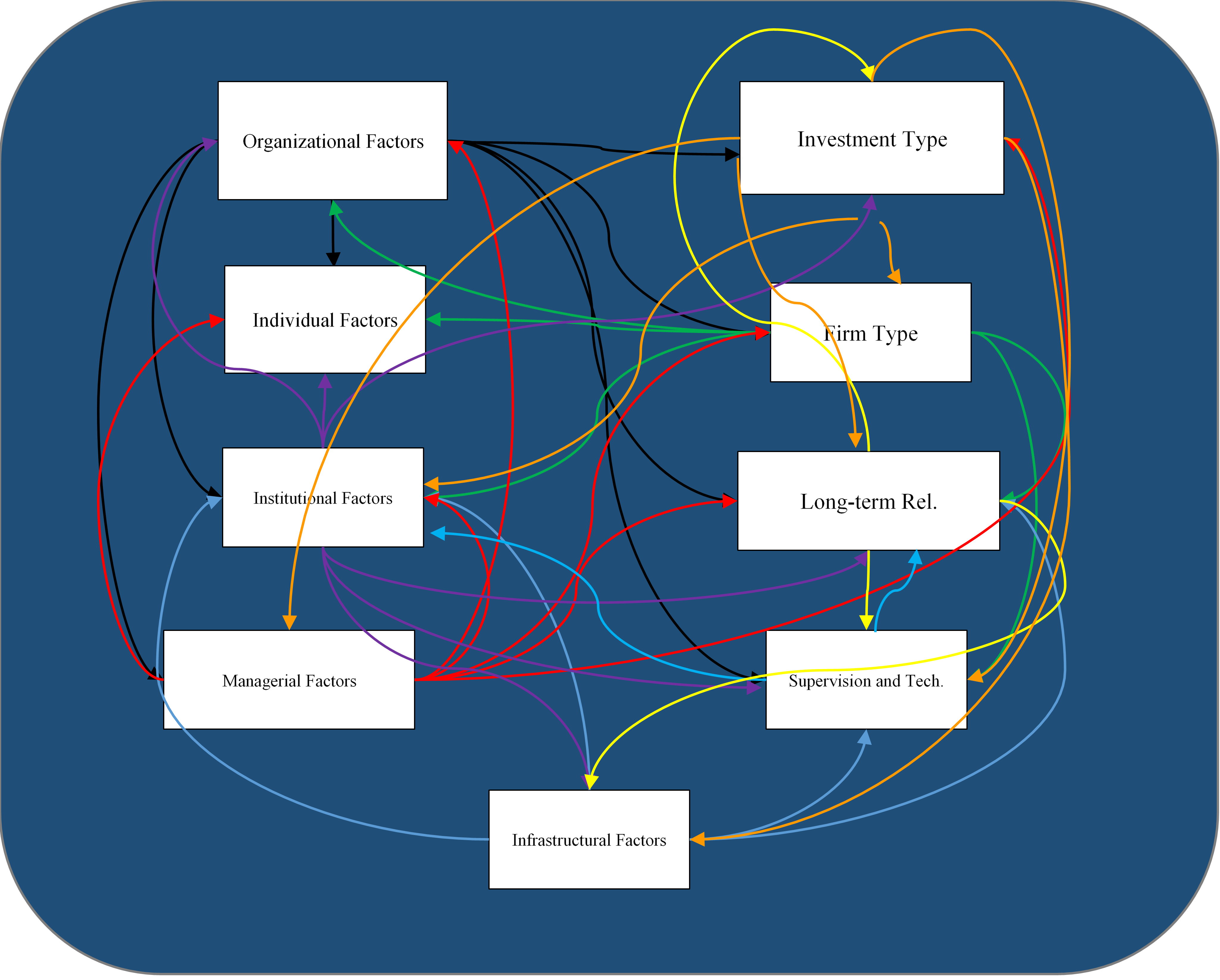

The present study aims to develop a model for audit documentation quality using internet-based technologies based on a grounded theory approach. Methodologically, the study is descriptive-analytical and, in terms of its purpose, practical. Data collection methods include library research and field studies. In the qualitative phase, data collection tools included observations and interviews, while in the quantitative phase, a questionnaire was employed. The qualitative statistical population consisted of experts and specialists affiliated with the Iranian Association of Auditing. Data analysis from each in-depth interview was conducted using purposive snowball sampling until theoretical saturation and data adequacy were achieved (20 interviews were conducted to reach theoretical saturation). Sampling in the qualitative phase was performed non-probabilistically and purposively. In the quantitative phase of the study, aimed at validating the final model, the statistical population included all auditors from selected and accredited firms. The sample size for this phase was calculated using Cochran's formula, resulting in 373 participants. A combination of qualitative and quantitative methods was employed for analysis. In the qualitative phase, in-depth interview techniques were used, and in the quantitative phase, interpretive structural modeling (ISM), structural equations modeling (SEM), and fuzzy DEMATEL and fuzzy ANP techniques were applied. Using the interview technique, nine criteria were identified, and strategies for audit documentation quality using internet-based technologies were proposed based on a grounded theory approach. Interpretive structural modeling and structural equations modeling elucidated the relationships between variables and the preliminary model framework. The fuzzy DEMATEL results revealed that "organizational factors" had the most significant impact on audit documentation quality using internet-based technologies compared to other factors, with "managerial factors" ranking second. Additionally, "supervisory and technological factors" were the most influenced by other factors. Fuzzy ANP results indicated that organizational factors were the highest priority, followed by long-term relationships, with other criteria ranking third.

References

L. S. D. Prado, "BRK: Digital Transformation to Delight Consumers," Cadernos Ebape Br, vol. 22, no. 2, 2024, doi: 10.1590/1679-395120230171x.

T. Wahyono, "Digital Transformation in MSMEs in Indonesia: The Importance of Commitment to Change," International Journal of Social Service and Research, vol. 4, no. 01, pp. 378-384, 2024, doi: 10.46799/ijssr.v4i01.703.

L. JiaYing, "Branding in Digital Transformation: Optimizing Multichannel Marketing Strategies With Big Data and Consumer Behavioral Analytics," Kuey, 2024, doi: 10.53555/kuey.v30i6.3412.

R. Zimmermann, A. Soares, and J. B. Roca, "The moderator effect of balance of power on the relationships between the adoption of digital technologies in supply chain management proces ses and innovation performance in SMEs," Industrial Marketing Management, vol. 118, pp. 44-55, 2024/4/1/ 2024, doi: 10.1016/J.INDMARMAN.2024.02.004.

A. A. Sahib and A. M. A. Wahhab, "Employ Successful Intelligence to Raise the Internal Auditor's Ability to Assess Risks: Evidence," 2023.

A. Saqafi and M. Jamalian Pour, "Technology, Blockchain, and the Future of Accounting and Auditing," Accountant, no. 9, 2018.

B. Mashayekhi, K. Mehrani, A. Rahmani, and A. Madani, "Developing an Auditing Quality Model," Securities Exchange Quarterly, vol. 6, no. 23, 2013.

A. A. Motaghi, A. Mohammadi, and M. Hashtami, "The Independence of the Board of Directors and Auditing Quality," in First National Conference on Auditing and Financial Supervision of Iran, 2016.

A. S. Soltani Nejad, O. Pour Heydari, and E. Soltani Nejad, "The Effect of Auditor Partner Workload on Auditing Quality, Auditor Report Delay, and Cost of Capital," Empirical Accounting Research, 2023.

Z. Hajiah, "Auditing Quality; There is Room for Improvement," Auditor Journal, no. 96, pp. 38-34, 2018.

Z. Hajiah and Z. Hamysian Kashani, "Presenting a Model to Increase the Quality of Auditing Documentation Based on Ethical Intelligence, Spiritual Intelligence, and Behavioral Background of Audit Partners," Journal of Financial Accounting Knowledge, vol. 11, no. 1, pp. 30-1, 2024.

M. F. Izzo, M. Fasan, and R. Tiscini, "The Role of Digital Transformation in Enabling Continuous Accounting and the Effects on Intellectual Capital: The Case of Oracle," Meditari Accountancy Research, 2021, doi: 10.1108/MEDAR-02-2021-1212.

M. J. A. Gonçalves, A. C. F. da Silva, and C. G. Ferreira, "The Future of Accounting: How Will Digital Transformation Impact the Sector?," Informatics, vol. 9, no. 1, p. 19, 2022, doi: 10.3390/informatics9010019.

L. Chu, H. Fogel-Yaari, and P. Zhang, "The Estimated Propensity to Issue Going Concern Audit Reports and Audit Quality," Journal of Accounting, Auditing & Finance, vol. 39, no. 2, 2024, doi: 10.1177/0148558X221079011.

H. Han, R. K. Shiwakoti, R. Jarvis, C. Mordi, and D. Botchie, "Auditing with Blockchain Technology and Artificial Intelligence: A Literature Review," International Journal of Accounting Information Systems, vol. 48, 2023, doi: 10.1016/j.accinf.2022.100598.

M. Delbari Raghab and A. Ismailzadeh Maghri, "Independent Auditing Quality Model Emphasizing Stakeholder Needs," Journal of Financial Accounting and Auditing Research, vol. 15, no. 1, pp. 98-69, 2023.

Q. Barzegar and A. Ahmadi, "Auditing in the Blockchain World," in Fourth National Conference on Research in Accounting and Management, 2020.

J. Barzgeri, S. M. Salehi Vaziri, and F. Gholabash, "Digital Transformation in the Area of Financial Reporting of Companies," in 18th National Accounting Conference of Iran, 2020.

G. R. Guşe and M. D. Mangiuc, "Digital Transformation in Romanian Accounting Practice and Education: Impact and Perspectives," Amfiteatru Economic, vol. 24, no. 59, pp. 252-267, 2022, doi: 10.24818/EA/2022/59/252.