Presenting the Management Accounting Model in the Digital Era

Keywords:

management accounting,, digital era, data-driven decision making, artificial intelligence algorithmsAbstract

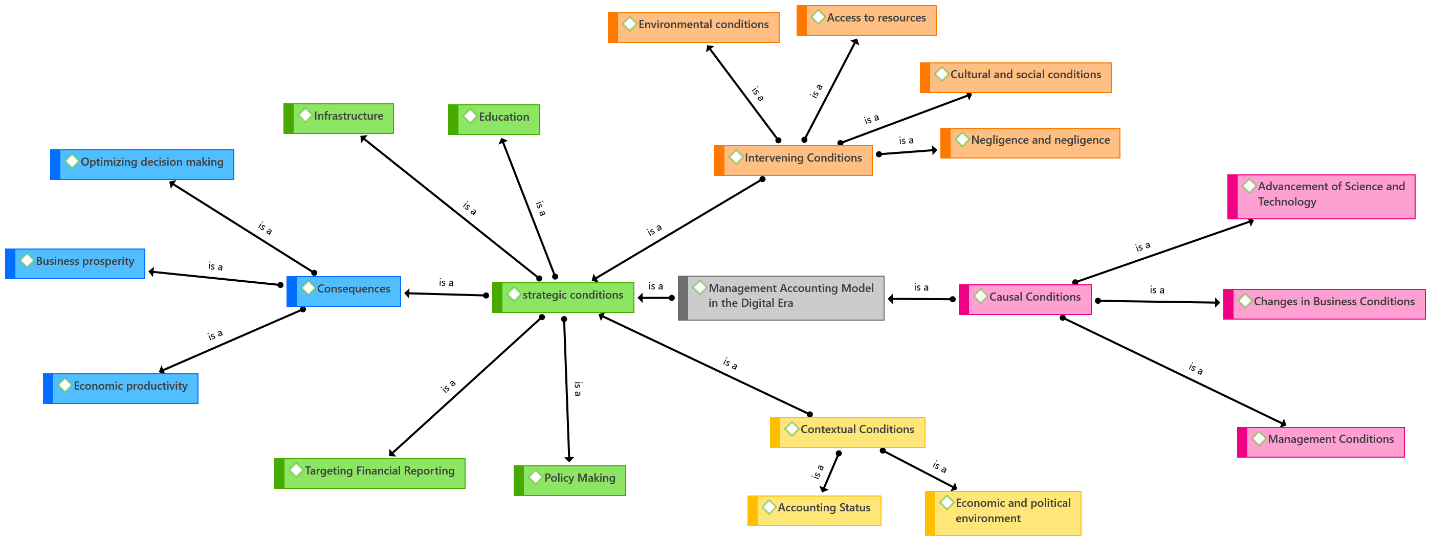

Digital technologies, including artificial intelligence and data analytics, have empowered organizations to make decisions with increased accuracy and speed. The objective of this study was to develop a management accounting model tailored to the demands of the digital era. This research is applied in nature and employed a qualitative methodology grounded in grounded theory. Data were collected through a combination of library research, reviews of specialized academic sources, and semi-structured interviews. Purposeful sampling was used to select 20 participants, including managers and shareholders from the stock exchange as well as financial management experts, during the year 2023. The interview data were coded using ATLAS.ti software. To ensure the validity of the findings, the data underwent qualitative analysis using three classification stages. The results were organized into five categories: causal, contextual (background), intervening, strategic, and consequential. The final model consists of six overarching categories and 16 core codes derived from 109 initial codes. Causal conditions included scientific and technological advancements, along with changes in business and managerial environments. Strategies identified in the model involved the development of education systems, infrastructure enhancement, and targeted financial reporting and policy-making. The consequences of implementing this model included improved decision-making efficiency, enhanced business growth, and increased economic productivity. Contextual conditions encompassed the broader economic and political landscape and the current state of accounting practices. Intervening conditions involved factors such as institutional negligence, cultural and societal influences, accessibility of resources, and environmental determinants. In the digital era, access to vast amounts of high-quality data has enabled more precise analysis. The proposed data-oriented management accounting model—leveraging data analytics tools and artificial intelligence—has significantly improved the precision of financial and strategic decision-making. This approach provides managers with more reliable and actionable insights, thereby enhancing organizational performance and supporting the achievement of long-term objectives.

References

H. Sun, "Construction of integration path of management accounting and financial accounting based on big data analysis," Optik, vol. 272, 2023, doi: 10.1016/j.ijleo.2022.170321.

Z. Bao, K. Hashim, and A. Almagrabi, "Business intelligence impact on management accounting development given the role of mediation decision type and environment," Information Processing & Management, vol. 60, 2023, doi: 10.1016/j.ipm.2023.103380.

A. A. Vărzaru, "Assessing artificial intelligence technology acceptance in managerial accounting," Electronics, vol. 11, no. 14, 2022, doi: 10.3390/electronics11142256.

A. Bhimani, "Digital data and management accounting: why we need to rethink research methods," Journal of management control, vol. 31, no. 1, pp. 9-23, 2020, doi: 10.1007/s00187-020-00295-z.

E. Tajvidi and S. Mohammadi, "The role of management accounting information in management control system in large manufacturing companies in Iran," Management Accounting, vol. 13, no. 46, pp. 1-16, 2020.

J. Ojra, A. P. Opute, and M. M. Alsolmi, "Strategic management accounting and performance implications: a literature review and research agenda," Future Business Journal, vol. 7, no. 1, p. 64, 2021, doi: 10.1186/s43093-021-00109-1.

P. Mikalef and E. Parmiggiani, "An Introduction to Digital Transformation," in Digital Transformation in Norwegian Enterprises. Cham: Springer, 2022.

A. Baiyere, H. Salmela, and T. Tapanainen, "Digital transformation and the new logics of business process management," European Journal of Information Systems, vol. 29, no. 3, pp. 238-259, 2020, doi: 10.1080/0960085X.2020.1718007.

C. Collins, D. Dennehy, K. Conboy, and P. Mikalef, "Artificial intelligence in information systems research: A systematic literature review and research agenda," International Journal of Information Management, vol. 60, 2021, doi: 10.1016/j.ijinfomgt.2021.102383.

F. Qiu, N. Hu, P. Liang, and K. Dow, "Measuring management accounting practices using textual analysis," Management Accounting Research, vol. 58, 2023, doi: 10.1016/j.mar.2022.100818.

Z. Huang, Savita, and A. K. Omar, "The impact of business intelligence on the marketing with emphasis on cooperative learning: Case-study on the insurance companies," Information Processing and Management, vol. 59, pp. 102-124, 2022, doi: 10.1016/j.ipm.2021.102824.

I. Goldstein, S. Yang, and L. Zuo, "The real effects of modern information technologies: Evidence from the EDGAR implementation," Journal of Accounting Research, vol. 61, no. 5, pp. 1699-1733, 2023, doi: 10.1111/1475-679X.12496.

K. Chang, A. A. Lasyoud, and D. Osman, "Management accounting system: Insights from the decision making theories," Social Sciences & Humanities Open, vol. 8, no. 1, 2023, doi: 10.1016/j.ssaho.2023.100529.

N. Melnyk, D. Y. Trachova, O. Kolesnikova, O. Demchuk, and N. Golub, "Accounting trends in the modern world," Independent Journal of Management & Production, vol. 11, no. 9, pp. 2403-2416, 2020, doi: 10.14807/ijmp.v11i9.1430.

S. Sule, N. Z. M. Yusof, and K. M. K. Bahador, "Users’ Perceptions on Auditors’ Responsibilities for Fraud Prevention, Detection and Audit Expectation GAP in Nigeria," Asian Journal of Economics, Business and Accounting, pp. 1-10, 2019, doi: 10.9734/AJEBA/2019/46832.

N. Takhtai, M. Shalalnejad, and A. Shalalnejad, "Digital technology and financial reporting," Accounting and Management Perspective, vol. 6, no. 82, pp. 187-191, 2022.

V. Mennati and A. Sasanian, "Skills, Influence, and Effectiveness of Management Accountants," Journal of Accounting Advances, vol. 14, no. 1, pp. 311-343, 2022, doi: 10.22099/jaa.2022.43316.2228.

M. Suleimanian and B. Bani Talebi Dehkordi, "The role of digital innovation in financial markets from the perspective of knowledge and presentation of the proposed model," Advances in Finance and Investment, vol. 4, no. 1, pp. 55-82, 2022.

A. Bhimani, Accounting disrupted: The reshaping of financial intelligence in the new digital era. New York: Wiley, 2020.

I. Posadzińska and M. Grzeszczak, "Management accounting system in the management of an intelligent energy sector enterprise," Energies, vol. 15, no. 20, 2022, doi: 10.3390/en15207633.

H. Salman Zadeh, G. Kordestani, and H. Kazemi, "The Role of Management Accounting in Improving Management Control System in Public Sector," Iranian Journal of Finance, vol. 6, no. 1, pp. 54-82, 2022, doi: 10.30699/ijf.2021.279013.1211.

R. Wadan, F. Teuteberg, F. Bensberg, and G. Buscher, "Understanding the changing role of the management accountant in the age of industry 4.0 in Germany," 2019, doi: 10.24251/HICSS.2019.702.