Systemic Risk Assessment of the Capital Market: Based on the Decomposition of Oil Shock Effects in the SVAR-Copula-GARCH Framework

Keywords:

systemic risk, capital market, oil shock, SVAR-Copula-GARCH frameworkAbstract

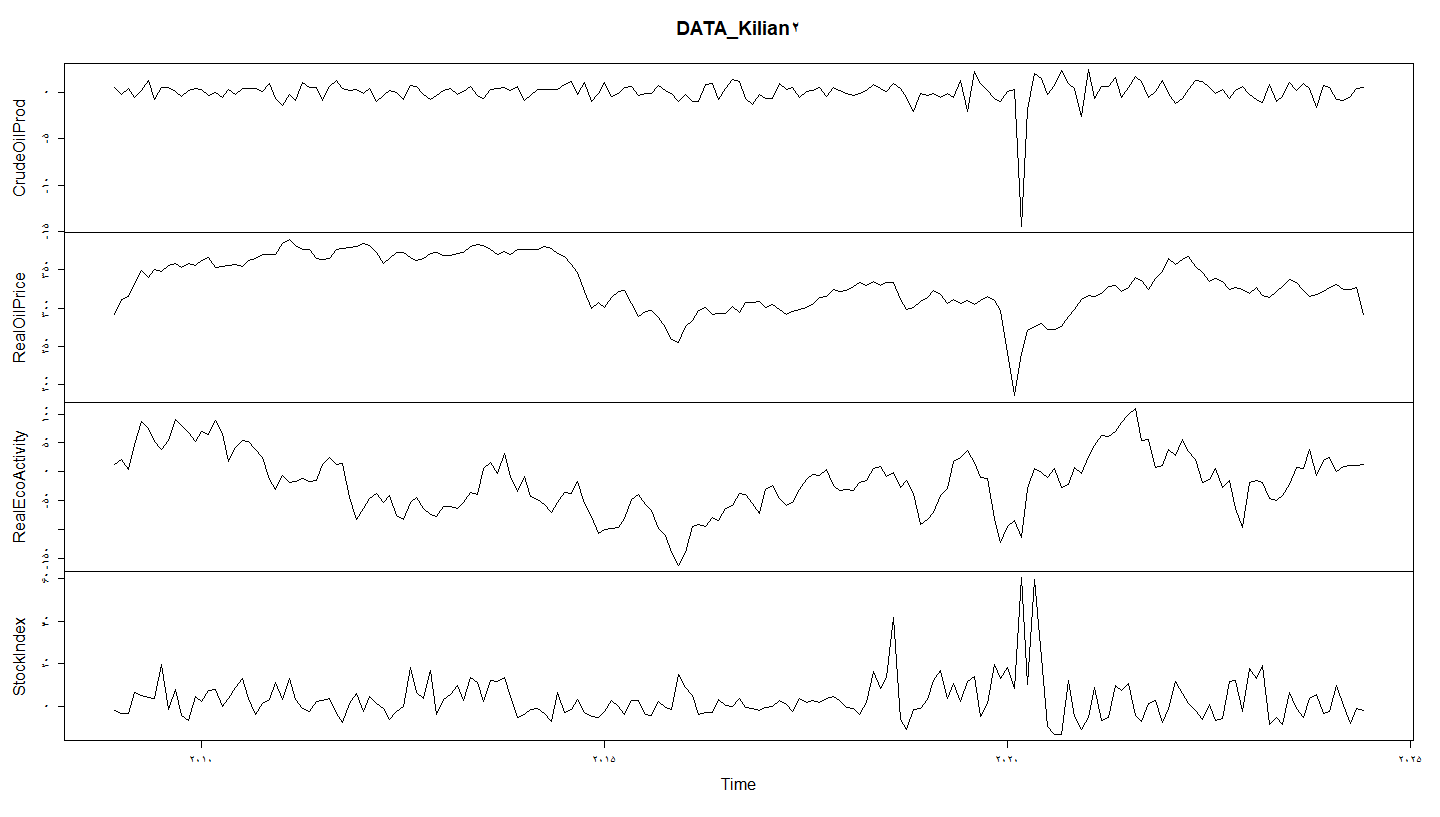

The specific oil shocks also exhibited the lowest Akaike criterion values under a normal distribution. Analyzing the results of the copula model under the Student’s t-distribution revealed that significant risk spillovers exist between the two markets during all three types of shocks. However, regarding oil supply shocks, the results confirm the presence of spillover effects from oil supply shocks to the stock market, and the 95% Value at Risk (VaR) is higher than the corresponding conditional CoVaR at the same probability level. This indicates that risk spillover from the oil market supply is associated with lower levels of value at risk in the stock market. Regarding demand-side shocks and specific oil shocks, it was also observed that significant and asymmetric risk spillover effects from the oil market to stock returns are statistically significant and confirmable. The Expected Shortfall (ES) results, except for supply shocks, were consistent with the conditional Value at Risk calculations. In fact, for all three types of oil supply shocks, the ES value is higher at the 95% level, but at the 5% level, the conditional expected shortfall is greater. This, despite confirming the existence of risk spillover effects, suggests that the spillover of oil supply shocks to the stock market is not symmetric. The spillover effects have varied across different levels of market risk exposure, indicating a long-term interpretation of shock spillover effects. Additionally, increasing and decreasing values of supply shocks have not had the same impact on stock returns.

References

L. Sakhaeipour, s. A. Ahmadi, A. Jamshidi, and M. Dalir, "Designing a talent management model of the National Iranian South Oilfield Company," (in eng), Strategic studies in the oil and energy industry, Research vol. 14, no. 56, pp. 133-154, 2023. [Online]. Available: http://iieshrm.ir/article-1-1485-en.html.

T. Mehrabi, T. Mojibi, and S. A. Safari Sabet, "Presenting an Organizational Productivity Measurement Model (Case Study: National Iranian Oil Company)," Strategic Studies in the Oil and Energy Industry Quarterly, vol. 15, no. 58, pp. 99-118, 2023. [Online]. Available: http://iieshrm.ir/article-1-1573-en.html.

E. Rasoulinezhad and M. Karimpour, "Characteristics and Aspects of the Oil Revenue Management Models in Iran and the Russian Federation," Transbaikal State University Journal, vol. 28, no. 5, pp. 101-109, 2022, doi: 10.21209/2227-9245-2022-28-5-101-109.

S. Mamipour, S. Yazdani, and E. Sepehri, "Examining the Spillover Effects of Volatile Oil Prices on Iran’s Stock Market Using Wavelet-Based Multivariate GARCH Model," Journal of Economics and Finance, vol. 46, no. 4, pp. 785-801, 2022, doi: 10.1007/s12197-022-09587-7.

S. M. Bisetoni, K. F. Hafshejani, A. Alirezaei, and G. A. Esfadan, "Exchange Rate Movements and Monetary Policies: Which Has Greater Influence on Petroleum," Iranian Journal of Finance, vol. 5, no. 1, pp. 147-172, 2021, doi: 10.30699/ijf.2021.125534.

M. Nonejad, Roozitalab, Anahita "The Effects of Economic Growth and Energy Consumption on Environmental Pollution: A Case Study of Iran," Journal of Environmental and Natural Resource Economics, vol. 2, no. 3, pp. 99-124, 2018, doi: 10.22054/eenr.2017.9069.

S. Rajabi, M. S. Shahdani, M. ZahediVafa, and G. Godarzi, "Hybrid Modeling of Natural Gas Allocation Amid Imbalances: Insights From Policy Scenarios in Iran," 2025, doi: 10.21203/rs.3.rs-5866982/v1.

E. Jahangard, A. Faridzad, M. Mousavi, and S. Matin, "Determining the Optimal Price of Natural Gas in Iran's Energy Market: Presenting a Computable General Equilibrium Model," Applied Economic Theories, vol. 10, no. 3, pp. 1-34, 2023.

N. Hashemi and H. Darvish, "Identifying dimensions and components of work-life balance among Employees of National Iranian Gas Company," Career and Organizational Counseling, vol. 15, no. 1, pp. 87-118, 2023, doi: 10.48308/jcoc.2023.103319.

H. Baki Haskoʾi and S. Samadi, "Estimating Portfolio Investment Variance Using Conditional GARCH Copula Models," in Third Conference on Financial Mathematics and Applications, Tehran, 2012.

H. Abbasi Nejad and S. Ebrahimi, "The Effect of Oil Price Volatility on the Returns of the Tehran Stock Exchange," Quarterly Journal of Economic Research and Policies, vol. 21, no. 68, pp. 83-103, 2013.

S. Homayounifar and A. Karimzadeh, "Investigating the Dynamic Correlation Between Major Assets in Iran Using the DCC-GARCH Method," Scientific-Research Quarterly on Economic Studies (Growth and Sustainable Development), vol. 13, no. 2, pp. 183-201, 2015.

M. H. Bot Shekan, M. Sadeqi-Shahdani, M. J. Salimi, and H. Mohseni, "Spillover of Fluctuations in the Stock Exchange," Quarterly Journal of Economic Research and Policies, vol. 25, no. 84, pp. 165-189, 2017.

Q. Ji, E. Bouri, D. Roubaud, and S. J. H. Shahzad, "Risk spillover between energy and agricultural commodity markets: A dependence-switching CoVaR-copula model," Energy Economics, vol. 75, pp. 14-27, 2018, doi: 10.1016/j.eneco.2018.08.015.

Q. Ji, B.-Y. Liu, and Y. Fan, "Risk dependence of CoVaR and structural change between oil prices and exchange rates: A time-varying copula model," Energy Economics, vol. 77, pp. 80-92, 2019, doi: 10.1016/j.eneco.2018.07.012.

Q. Ji, B.-Y. Liu, H. Nehler, and G. S. Uddin, "Uncertainties and extreme risk spillover in the energy markets: A time-varying copula-based CoVaR approach," Energy Economics, vol. 76, pp. 115-126, 2018, doi: 10.1016/j.eneco.2018.10.010.

W. Mensi, S. Hammoudeh, S. J. H. Shahzad, and M. Shahbaz, "Modeling systemic risk and dependence structure between oil and stock markets using a variational mode decomposition-based copula method," Journal of Banking & Finance, vol. 75, pp. 258-279, 2017, doi: 10.1016/j.jbankfin.2016.11.017.

C. Peng, H. Zhu, Y. Guo, and X. Chen, "Risk spillover of international crude oil to China's firms: Evidence from granger causality across quantile," Energy Economics, vol. 76, 2018, doi: 10.1016/j.eneco.2018.04.007.

J. Huang, Z. Li, and X. Xia, "Network diffusion of international oil volatility risk in China's stock market: Quantile interconnectedness modelling and shock decomposition analysis," International Review of Economics & Finance, vol. 76, pp. 1-39, 2021, doi: 10.1016/j.iref.2021.04.034.

B. Lin, P. K. Wesseh, and M. O. Appiah, "Oil price fluctuation, volatility spillover and the Ghanaian equity market: Implication for portfolio management and hedging effectiveness," Energy Economics, vol. 40, pp. 825-831, 2014, doi: 10.1016/j.eneco.2013.12.017.

L. Yu, R. Zha, D. Stafylas, K. He, and J. Liu, "Dependences and volatility spillovers between the oil and stock markets: New evidence from the copula and VAR-BEKK-GARCH models," International Review of Financial Analysis, vol. 68, 2020, doi: 10.1016/j.irfa.2018.11.007.

M. Zolfaghari, H. Ghoddusi, and F. Faghihian, "Volatility spillovers for energy prices: A diagonal BEKK approach," Energy Economics, vol. 92, 2020, doi: 10.1016/j.eneco.2020.104965.

A. A. Salisu, R. Demirer, R. Gupta, J. M. Sangeetha, and K. J. Alfia, "Technological shocks and stock market volatility over a century Financial stock market forecast using evaluated linear regression based machine learning technique," Journal of Empirical Finance, vol. 79, p. 101561, 2024, doi: 10.1016/j.measen.2023.100950.

A. H. A. Rady, F. Essam, H. Yahia, and M. Shalaby, "The Dynamic Relationship Between Exchange Rate Volatility and Stock Prices in the Egyptian Real Estate Market and the Moderating Effect of Interest Rates," European Journal of Business Management and Research, vol. 9, no. 5, pp. 31-44, 2024, doi: 10.24018/ejbmr.2024.9.5.2230.

J. Mugendi, "Impact of Macroeconomic Variables on Stock Market Volatility in Kenya," American Journal of Finance, vol. 10, no. 1, pp. 59-71, 2024, doi: 10.47672/ajf.1812.

M. Eyshi Ravandi, M. Moeinaddin, A. Taftiyan, and M. Rostami Bashmani, "Investigating the Impact of Investor Sentiment and Liquidity on Stock Returns of the Iranian Stock Exchange," (in en), Dynamic Management and Business Analysis, vol. 3, no. 1, pp. 40-52, 2024, doi: 10.22034/dmbaj.2024.2038046.1068.

B. Dhingra, S. Batra, V. Aggarwal, M. Yadav, and P. Kumar, "Stock market volatility: a systematic review," Journal of Modelling in Management, vol. 19, no. 3, pp. 925-952, 2024, doi: 10.1108/JM2-04-2023-0080.

I. Hasanzadeh, M. J. Sheikh, M. Arabzadeh, and A. A. Farzinfar, "The Role of Economic Policy Uncertainty in Relation to Financial Market Instability and Stock Liquidity in Tehran Stock Exchange Companies," (in en), Dynamic Management and Business Analysis, vol. 2, no. 3, pp. 163-178, 2023, doi: 10.22034/dmbaj.2024.2031971.2315.

N. Seifollahi and H. Seifollahi Anar, "Examining the Mechanism of the Impact of Exchange Rate Fluctuations, Oil Prices, and Economic Growth on the Overall Tehran Stock Exchange Index," Financial Economics, vol. 15, no. 55, pp. 333-353, 2021. [Online]. Available: https://www.magiran.com/paper/2371909/investigating-the-mechanism-of-fluctuation-exchange-rate-oil-price-and-economic-growth-on-the-tehran-securities-exchange?lang=en.

S. Zein al-Dini, M. Sharif-Karimi, and A. Khanzadi, "Examining the Impact of Oil Price Shocks on the Performance of the Iranian Stock Market," Financial Economics Quarterly, vol. 14, no. 50, pp. 145-170, 2020.

M. H. Fotros and M. Hoshidari, "The effect of crude oil price volatility on volatility in Tehran stock market GARCH multivariate approach," Iranian Energy Economics, vol. 5, no. 18, pp. 147-177, 2016. [Online]. Available: https://jiee.atu.ac.ir/article_7195_en.html.

Downloads

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2025 Neda Rezaee (Author); Shahram Chaharmahali (Corresponding author); Mohammad Kohandel, Nowrouz Nourollahzade (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.