Providing a Continuous Risk-Monitoring Model in the Banking Sector Based on Grounded Data

Keywords:

Continuous monitoring, banking sector, grounded dataAbstract

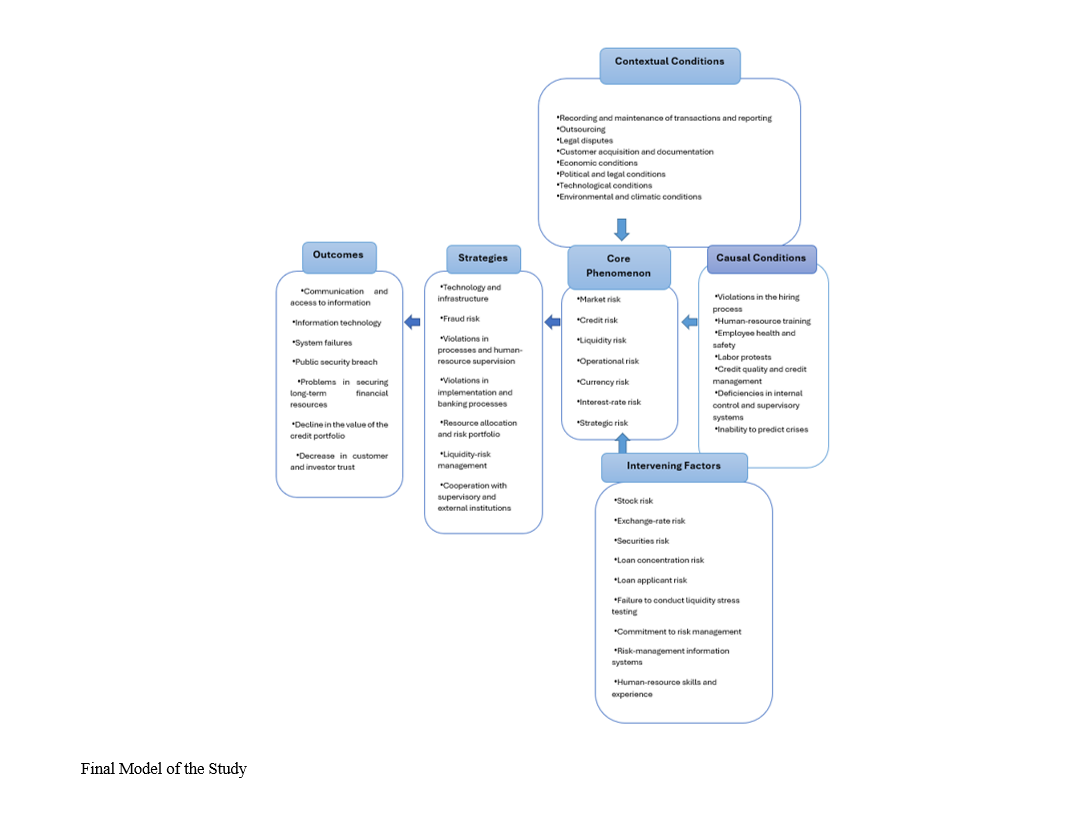

The purpose of this study is to present a model for continuous risk monitoring in the banking sector based on grounded data. The damage resulting from the non-payment of the principal or interest of a loan is referred to as credit risk. Collateral and guarantees in debt contracts play several roles, including protecting the interests of lenders in the event of default. Moreover, collateral helps improve lending conditions by reducing moral hazard and information asymmetry between lenders and borrowers. In the meta-synthesis stage, a theoretical–deductive analysis is conducted as the first step in the multi-grounded theory approach. The objective of this step is to identify valid, credible, and relevant documents within an appropriate time frame. To this end, articles, books, and reputable national and international organizational websites were reviewed. The first step in meta-synthesis involves formulating the research questions based on the dimensions of grounded theory. In the second step, the researcher systematically searches published articles in reputable domestic and international scientific journals to determine valid and credible documents within the appropriate period. Initially, relevant keywords—individually or in combination—were examined in both Persian and English for the years 2013 to 2024, and for English-language articles for the years 1980 to 2023. Ultimately, 34 articles were identified. The research data were analyzed using a coding method, and the main categories and concepts were extracted. A conceptual model was developed through which the components related to continuous risk monitoring in the banking sector were identified. Based on this model, the most important causal conditions that may influence banking-sector risk include market risk, credit risk, liquidity risk, operational risk, currency risk, interest rate risk, and strategic risk. The research model showed that continuous risk monitoring in the banking sector may lead to consequences such as communication and access to information issues, information technology and system failures, public security breaches, challenges in obtaining long-term financing, reduction in the value of the credit portfolio, and decreased customer and investor trust.

References

[1] K. Pam and R. Neygouan, "Global market integration: An alternative measure and its application," Journal of financial economics, vol. 94, no. 2, pp. 214-232, 2025, doi: 10.1016/j.jfineco.2008.12.004.

[2] M. M. Adam, D. B. Salleh, and W. Waemustafa, "Empirical examination of credit risk determinant of commercial banks in Jordan," Risks, vol. 10, no. 4, p. 85, 2024, doi: 10.3390/risks10040085.

[3] B. Maghiebereh, M. Yimani, and F. Aliu, "Relationship banking, collateral, and the economic crisis as determinants of credit risk: an empirical investigation of SMEs," The South East European Journal of Economics and Business, vol. 18, no. 2, pp. 49-62, 2023, doi: 10.2478/jeb-2023-0018.

[4] R. B. Abdesslem, I. Chkir, and H. Dabbou, "Is managerial ability a moderator? The effect of credit risk and liquidity risk on the likelihood of bank default," International Review of Financial Analysis, vol. 80, p. 102044, 2022, doi: 10.1016/j.irfa.2022.102044.

[5] O. K. Natufe and E. I. Evbayiro-Osagie, "Credit risk management and the financial performance of deposit money banks: some new evidence," Journal of Risk and Financial Management, vol. 16, no. 7, p. 302, 2023, doi: 10.3390/jrfm16070302.

[6] T. Wang and C. Hsu, "Board composition and operational risk events of financial institutions," Journal of Banking & Finance, vol. 37, no. 6, pp. 2042-2051, 2013, doi: 10.1016/j.jbankfin.2013.01.027.

[7] A. Mor -Valencia and W. Zapata-Jaramillo, "Quantifying operational risk using the loss distribution approach (lda) model," in Proceedings of the Seventh European Academic Research Conference on Global Business, Economics, Finance and Banking (EAR17Swiss Conference), 2022, pp. 0-10.

[8] M. Nāderī, M. A. Rastgār Surkheh, B. Ostādī, and M. Kārgarī, "Predicting the Probability of Operational Risk Occurrence in the Banking Industry Using Machine Learning Algorithms," Asset and Financing Management Quarterly, vol. 13, no. 4, pp. 77-96, 2025.

[9] S. M. Tabāṭabā'ī, S. N. Makkiyān, and Z. Naṣrollāhī, "The Effects of Shadow Banking on Banking Risk Considering the Role of Capital Structure in Iran," Scientific Quarterly of Islamic Economics and Banking, no. 47, pp. 347-370, 2024.

[10] Y. Gūdarzī Farāhānī, Z. Mursalī Arzanaq, and M. Mehra'ārā, "Investigating the Relationship between Diversification of Bank Sources and Uses and Systemic Risk," Strategic Management Quarterly, vol. 12, no. 45, pp. 27-52, 2024.

[11] X. Liu et al., "A hybrid classification system for heart disease diagnosis based on the RFRS method," Computational and Mathematical Methods in Medicine, p. 8272091, 2017, doi: 10.1155/2017/8272091.

[12] Q. K. Nguyen, "The impact of risk governance structure on bank risk management effectiveness: Evidence from ASEAN countries," Heliyon, vol. 8, no. 10, 2022, doi: 10.1016/j.heliyon.2022.e11192.

[13] A. Yāvarī, H. Jabbārī, and H. Panāhiyān, "Designing a Credit Risk Management Model with a Pathological Approach to Guarantees and Collaterals of Bank Facilities," Technology in Entrepreneurship and Strategic Management Quarterly, vol. 4, no. 2, pp. 1-22, 2025, doi: 10.61838/kman.jtesm.4.2.11.

[14] M. Roshan and S. Khodarahmi, "Measuring Credit Risk and Capital Adequacy Considering the Size and Ownership Structure of Listed Banks in Iran Based on the Generalized Method of Moments (GMM) Panel Model," Management Accounting and Auditing Knowledge, vol. 14, no. 54, pp. 313-329, 2024.

[15] M. Naili and Y. Lahrichi, "The determinants of banks' credit risk: Review of the literature and future research agenda," International Journal of Finance & Economics, vol. 27, no. 1, pp. 334-360, 2022, doi: 10.1002/ijfe.2156.

[16] K. Mahrānī, S. F. Akbari Kiyārūdī, and A. Heydarī, "Developing a Framework for Implementing Comprehensive Risk Management in the Banking Industry (Multiple Case Study)," Empirical Accounting Research, vol. 14, no. 53, pp. 1-44, 2024.

[17] A. Feyz̄ī and M. Mūsawī, "Application of Bayesian Network Analysis in Bank Risk Management (Case Study: Bank Saderat Iran)," 2024.

Downloads

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2025 Soroosh Shanaki Bavarsad, Saeed Nasiri, Ahmad Kaab Omair, Allahkaram Salehi (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.