Identifying and prioritizing factors affecting the quality of internal controls

Keywords:

Quality, internal controls, board structure, proper documentation of procedures.Abstract

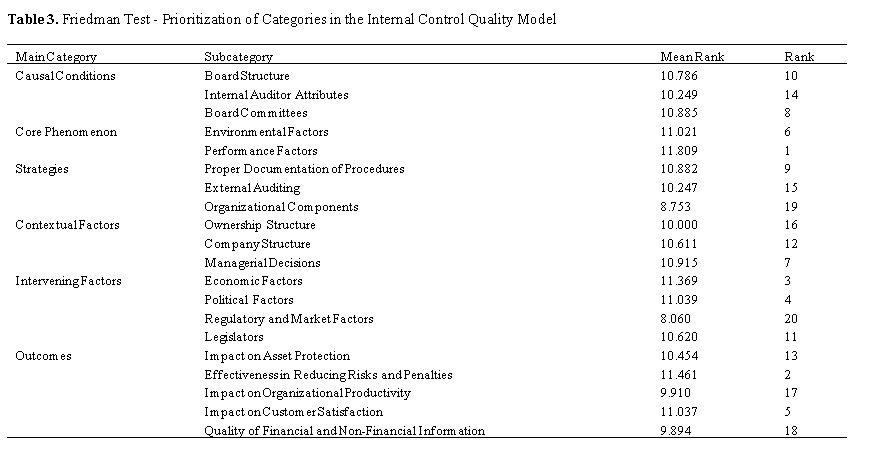

The aim of this research is to identify and prioritize factors affecting the quality of internal controls. To achieve this objective, a set of indicators and components related to the quality of internal controls were identified through a review of theoretical foundations and previous studies, as well as interviews with experts and professionals in the field. A qualitative research approach using a multiple-grounded theory method was applied. Therefore, data analysis was conducted at both the empirical and theoretical levels. The required empirical data was obtained through theoretical sampling of 15 semi-structured interviews with professionals who had successful experience in implementing the mentioned system during the years 2019 and 2023. The theoretical data was obtained through a literature review. The results of the qualitative research revealed several conditions and factors that influence the quality of internal controls. Causal conditions include the structure of the board, characteristics of internal auditors, and board committees. Core conditions refer to environmental factors and performance factors. Strategies, such as proper documentation of procedures, external auditing, and organizational components, emerged as key actions and interactions in improving internal control quality. Contextual factors include ownership structure, company structure, and managerial decisions. Intervening factors were identified as economic, political, regulatory, and market factors, as well as the role of legislators. The outcomes of the study highlight the impact of internal controls on asset protection, the efficiency of internal controls in reducing risks and penalties, the effect of internal controls on organizational productivity, customer satisfaction, and the overall quality of both financial and non-financial information.

References

W. Cheng, C. Li, and T. Zhao, "The stages of enterprise digital transformation and its impact on internal control: Evidence from China," International Review of Financial Analysis, vol. 92, p. 103079, 2024, doi: 10.1016/j.irfa.2024.103079.

R. A. Praja, "The Influence of Human Resources Audit and Internal Control System on Employee Performance in PT. Subur Sedaya Maju Prabumulih," JuBIR, vol. 2, no. 2, p. 115, 2024, doi: 10.31315/jubir.v2i2.7958.

Y. E. Rachmad, A. A. Bakri, S. Irdiana, J. Waromi, and A. A. J. Sinlae, "Analysis of The Influence of Financial Information Systems, Internal Control Systems, and Information Technology on Quality of Financial Reports," Jurnal Informasi Dan Teknologi, pp. 266-271, 2024, doi: 10.60083/jidt.v6i1.513.

B. A. F. Jarah, N. Zaqeeba, M. F. M. Al-Jarrah, A. M. Al Badarin, and Z. Almatarneh, "The mediating effect of the internal control system on the relationship between the accounting information system and employee performance in Jordan Islamic banks," Economies, vol. 11, no. 3, p. 77, 2023, doi: 10.3390/economies11030077.

H. Zhou, H. Chen, and Z. Cheng, "Internal control, corporate life cycle, and firm performance," in The Political Economy of Chinese Finance, vol. 17, M. R. P. X. T. Z. J. Jay Choi Ed., 2016, pp. 189-209.

M. Boulhaga, A. Bouri, A. A. Elamer, and B. A. Ibrahim, "Environmental, social and governance ratings and firm performance: The moderating role of internal control quality," Corporate Social Responsibility and Environmental Management, vol. 30, no. 1, pp. 134-145, 2023, doi: 10.1002/csr.2343.

H. Zhang and S. Dong, "Digital transformation and firms' total factor productivity: The role of internal control quality," Finance Research Letters, vol. 57, p. 104231, 2023, doi: 10.1016/j.frl.2023.104231.

A. Taheri, N. Shahmoradi, and M. Mo'in al-Din, "Identifying the Gap Between the Current Status and the Desired Level of Internal Control Structures in Executive Agencies of Fars Province," Auditing Knowledge, vol. 18, no. 70, pp. 105-130, 2018.

M. Khorram Abadi, Y. Hassas Yeganeh, F. Barzideh, and J. Salehi Sadeghiani, "Modeling Effectiveness Evaluation Indicators of Internal Controls in Companies Listed on Tehran Stock Exchange with a Structural-Interpretive Approach (ISM)," Auditing Knowledge, vol. 20, no. 78, pp. 223-259, 2020.

M. Jasemi, "Investigating the Effect of Audit Characteristics on the Effectiveness of Internal Control in Companies," Scientific Quarterly of Modern Research Approaches in Management and Accounting, vol. 4, no. 12, pp. 97-111, 2020.

H. Katiri and R. Sabri, Internal Control Framework for Independent Auditors. Official Auditors Society Publications, 2019.

Y. Hassas Yeganeh and G. Taghi Nataj Malekshah, "The Relationship Between Internal Control Reports and User Decision Making," Quarterly Journal of Empirical Studies in Financial Accounting, vol. 4, no. 14, pp. 133-176, 2006.

B. Jafari, R. Alikhani, M. Moranjouri, and M. R. Pourali, "Examining the Moderating Role of Managerial Narcissism in Explaining the Relationship Between Auditor Characteristics and Internal Control Effectiveness," Auditing Knowledge, vol. 22, no. 86, pp. 165-186, 2022.

X. D. Ji, W. Lu, and W. Qu, "Determinants and economic consequences of voluntary disclosure of internal control weaknesses in China," Journal of Contemporary Accounting & Economics, vol. 11, pp. 1-11, 2019, doi: 10.1016/j.jcae.2014.12.001.

A. A. Oussii and N. Boulila Taktak, "The impact of internal audit function characteristics on internal control quality," Managerial Auditing Journal, 2018, doi: 10.1108/MAJ-06-2017-1579.

M. Feng, C. Li, S. E. McVay, and H. A. Skaife, "Does ineffective internal control financial reporting affect a firm's operations? Evidence from firms' inventory over-management," The Accounting Review, vol. 90, no. 2, pp. 529-557, 2015, doi: 10.2308/accr-50909.

C. Liu, B. Lin, and W. Shu, "Employee quality, monitoring environment, and internal control in China," Journal of Accounting Research, pp. 51-70, 2017, doi: 10.1016/j.cjar.2016.12.002.

A. Bazarafshan, "The Impact of Audit Committee Quality on Achieving Internal Control Objectives Governing Financial Reporting," Empirical Studies in Financial Accounting, vol. 13, no. 52, pp. 179-284, 2016.

Y. Sun, "Internal control weakness disclosure and firm investment," Journal of Accounting Auditing & Finance, vol. 31, no. 2, pp. 277-307, 2016, doi: 10.1177/0148558X15598027.

M. Lotfalian and H. Vali Pour, "Studying the Effectiveness of the Internal Control System Designed in Niroo Trans Company," Knowledge of Accounting and Management Auditing, vol. 4, no. 16, pp. 1-14, 2014.

J. Luukkanen, M. Nevas, M. Fredriksson-Ahomaa, and J. Lundén, "Developing official control in slaughterhouses through internal audits," Food Control, vol. 90, pp. 344-351, 2018, doi: 10.1016/j.foodcont.2018.03.014.