Designing a Model of the Impact of Artificial Intelligence Capabilities in Accounting Systems on Reducing Errors in Financial Reports

Keywords:

Artificial Intelligence Capabilities, Accounting Systems, Reducing Errors in Financial ReportingAbstract

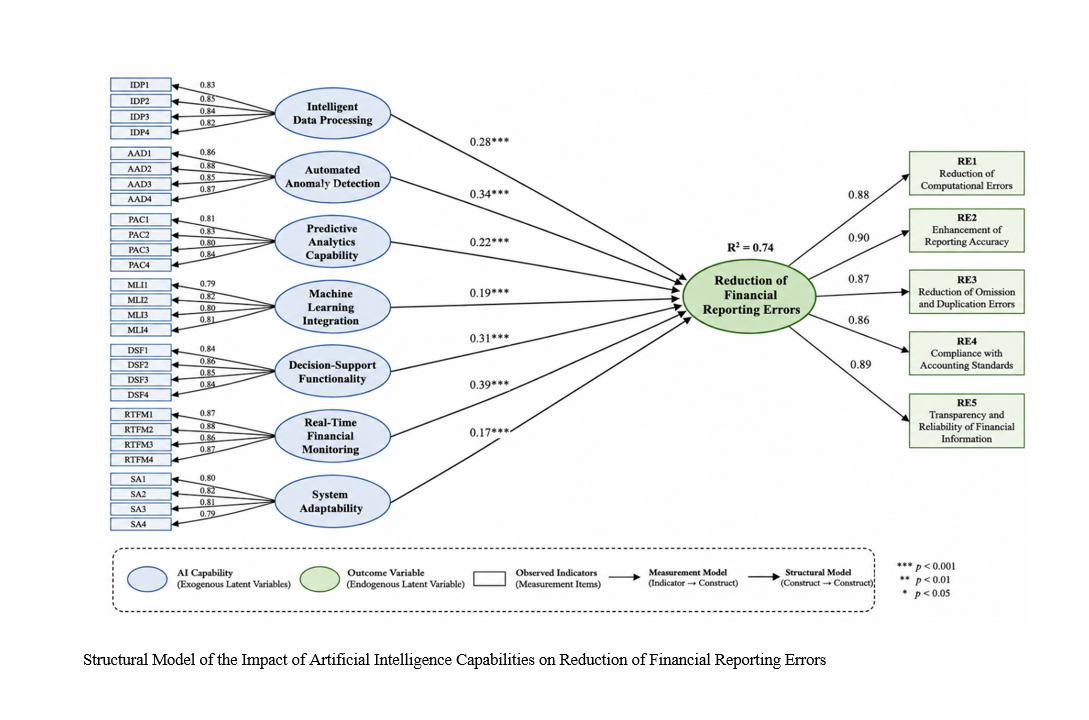

The present study aimed to design and validate a model explaining the impact of artificial intelligence capabilities in accounting systems on reducing financial reporting errors in organizations and financial institutions. This study was conducted using a mixed-methods exploratory sequential design. In the qualitative phase, semi-structured interviews were conducted with 18 university professors, financial managers, auditors, and accounting information system specialists in Tehran using purposeful and snowball sampling methods until theoretical saturation was achieved. The qualitative data were analyzed through thematic analysis and coding procedures using MAXQDA software. In the quantitative phase, the statistical population consisted of accountants, financial managers, auditors, and accounting system specialists employed in financial institutions and private companies in Tehran during 2026. Based on Cochran’s formula, 384 participants were selected through stratified random sampling. Data were collected using a researcher-developed questionnaire designed according to the qualitative findings and existing theoretical literature. The validity of the instrument was confirmed through expert evaluation and confirmatory factor analysis, while reliability was assessed using Cronbach’s alpha and composite reliability coefficients. Quantitative data were analyzed using SPSS version 27 and SmartPLS version 4 through descriptive statistics, confirmatory factor analysis, correlation analysis, and structural equation modeling. The findings demonstrated that all dimensions of artificial intelligence capabilities had significant positive effects on reducing financial reporting errors. Real-time financial monitoring had the strongest effect on reducing financial reporting errors (β = 0.39, p < 0.001), followed by automated anomaly detection (β = 0.34, p < 0.001), decision-support functionality (β = 0.31, p < 0.001), intelligent data processing (β = 0.28, p < 0.001), predictive analytics capability (β = 0.22, p < 0.001), machine learning integration (β = 0.19, p < 0.001), and system adaptability (β = 0.17, p < 0.001). The structural model exhibited satisfactory fit indices, and the coefficient of determination indicated that artificial intelligence capabilities explained 74% of the variance in reduction of financial reporting errors. The findings indicate that artificial intelligence capabilities significantly improve the accuracy, transparency, and reliability of financial reporting systems by enhancing monitoring processes, anomaly detection, predictive analysis, and intelligent decision-making. The study confirms that intelligent accounting technologies can substantially reduce financial reporting errors and strengthen organizational financial governance. Therefore, organizations are encouraged to invest in intelligent accounting infrastructures and develop technological readiness to improve financial reporting quality and operational efficiency.

References

[1] A. Mirzaei, "Artificial intelligence in accounting: Opportunities and challenges," Iranian Journal of Accounting Research, vol. 18, no. 2, pp. 45-61, 2025.

[2] M. I. Khan, A. Rahim, and S. Ullah, "The Use of Artificial Intelligence in Accounting Auditing: Challenges and Opportunities," Journal of Accounting and Finance, vol. 25, no. 1, pp. 78-95, 2025.

[3] S. Calado and C. M. Veloso, "Artificial Intelligence in Accounting: Driving Value Co-Creation, Compliance, and Ethical Transformation," in Empowering Value Co-Creation in the Digital Era: IGI Global Scientific Publishing, 2025, pp. 75-102.

[4] N. Sheikh, "The effect of applying artificial intelligence on financial reporting quality: The mediating role of user trust in accounting systems," Accounting, Finance and Computational Intelligence, 2025.

[5] E. Saadati, Z. Ansari, A. Farahmandnia, and K. Asadi Mehr, "A strategy-oriented approach to the application of artificial intelligence technology in accounting: With reference to auditing and management accounting trends," Strategic Management Accounting Quarterly, vol. 2, no. 2, pp. 1-20, 2025.

[6] O. Farhadi Touski and R. Doustian, "Developing New Technologies in Internal Auditing with the Help of Artificial Intelligence: Deep Learning Enables Anomaly Detection in Financial Accounting Data," Investment Knowledge, vol. 14, no. 55, pp. 597-612, 2025.

[7] T. Cao, J. Zhao, R. Wang, X. He, and P. Sun, "Research on the Application and Efficiency Improvement of Artificial Intelligence in Financial Accounting and Auditing," Journal of Computational Methods in Sciences and Engineering, 2025, doi: 10.1177/14727978241299644.

[8] R. Darabi and M. Dolatshahi, "The Effect of Artificial Intelligence on Budgeting Optimization and Financial Forecasting Accuracy in Management Accounting: A Case Study of Manufacturing Companies in Tehran Province," Strategic Management Accounting, vol. 2, no. 2, pp. 21-42, 2025, doi: 10.22034/smajournal.2025.518968.1014.

[9] M. Najari, "Analysis of financial costs using artificial intelligence," 2025: Paper presented at the Twenty-Fourth National Conference on Economics, Management, and Accounting. [Online]. Available: https://en.civilica.com/doc/2318809/.

[10] H. Abu-Khadra, M. Al-Okaily, and A. Al-Bashir, "Auditing in the Digital Age: The Role of Artificial Intelligence in Fraud Detection," Journal of Emerging Technologies in Accounting, vol. 22, no. 1, pp. 45-67, 2025, doi: 10.1108/ITSE-03-2025-0071.

[11] S. Khalafi, S. A. Pardehchi, and S. Solouki, "The role of artificial intelligence in transforming banking services: A conceptual model of interaction between AI-based security and customer loyalty in financial services," Perspective of Accounting and Management, vol. 8, no. 101, pp. 175-186, 2025. [Online]. Available: https://www.jamv.ir/article_227593.html.

[12] A. Saghafi and M. R. Parsapour, "Investigating the impact of accounting data analysis using generative artificial intelligence on the quality of digital sustainability reporting considering the mediating role of green sustainability internal control systems," Financial Accounting Knowledge, vol. 12, no. 1, pp. 1–31, 2025, doi: 10.30479/jfak.2025.21533.3270.

[13] B. Rostami Zabol, "Criminal liability arising from the actions of autonomous Artificial Intelligence in the Iranian criminal legal system: Challenges and legislative necessities," in 14th International and National Conference on Management, Accounting, and Law Studies, Tehran, 2025.

[14] H. Esmaeili Abdar, "Challenges and Consequences of Artificial Intelligence in Organizations," presented at the National Conference on Investment for Production with the Transformative Role of Accounting and Management, Meybod, 2025.

[15] B. Moshayekhi and M. R. Amirollah, "The Impact of Knowledge and Professional Skepticism of Internal Auditors on the Adoption of Artificial Intelligence," Experimental Accounting Research, vol. 15, no. 2, pp. 1-28, 2025, doi: 10.22051/jera.2025.50268.3523.

[16] B. Mashayekhi and S. Amrollahi, "Investigating factors affecting the adoption of artificial intelligence by internal auditors," Financial Accounting and Auditing Research, vol. 16, no. 61, pp. 23-48, 2025. [Online]. Available: https://jera.alzahra.ac.ir/article_8573.html.

[17] N. Jafari, "Investigating the Impact of Artificial Intelligence on Employee Performance and Work Engagement (Case Study: Urmia Municipality)," in The 14th International Conference on Interdisciplinary Research in Management, Accounting, and Economics in Iran, Tehran, 2025.

[18] M. Ali Mohammadi, "The Impact of Artificial Intelligence on Recruitment Processes and Smart Human Resource Attraction in Improving Organizational Performance," presented at the Eleventh International Conference on Management, Accounting, Banking, and Economics of Iran, Mashhad, 2025.

[19] M. Amirkhani Nia, P. Tohidi, and S. H. Mirzamani, "Investigating the Impact of Artificial Intelligence on the Academic Advancement of Female Students at Shahrekord Technical and Vocational College," Quarterly Journal of New Research Approaches in Management and Accounting, vol. 8, no. 92, pp. 847-858, 2025. [Online]. Available: https://majournal.ir/index.php/ma/article/view/2521.

[20] M. Adnan Hammoud, P. Piri, and A. Ashtab, "Feasibility study of utilizing modern artificial intelligence technologies to improve auditing processes in the country," Accounting and Auditing Reviews, vol. 32, no. 3, pp. 535-559, 2025, doi: 10.22059/acctgrev.2025.391837.1009085.

[21] J. K. Nembe, J. O. Atadoga, N. Z. Mhlongo, T. F. Falaiye, A. I. Daraojimba, and B. B. Oguejiofor, "The role of artificial intelligence in enhancing tax compliance and financial regulation," Finance & Accounting Research Journal, vol. 6, no. 2, p. Article 822, 2025, doi: 10.51594/farj.v6i2.822.

[22] M. Khaleghizadeh Dehkordi, F. Sarraf, and A. Najafi Moqaddam, "The Role of Performance Metrics in Explaining Investment Efficiency with Emphasis on Artificial Intelligence Method," Accounting and Management Auditing Knowledge, vol. 13, no. 51, pp. 151-168, 2025.

Downloads

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2025 Noshin Sheikh (Corresponding author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.