Proposing a Model of Forensic Accounting Tools to Reduce Financial Crimes

Keywords:

Forensic Accounting Tools, Fraud, Forensic Accounting, Financial CrimesAbstract

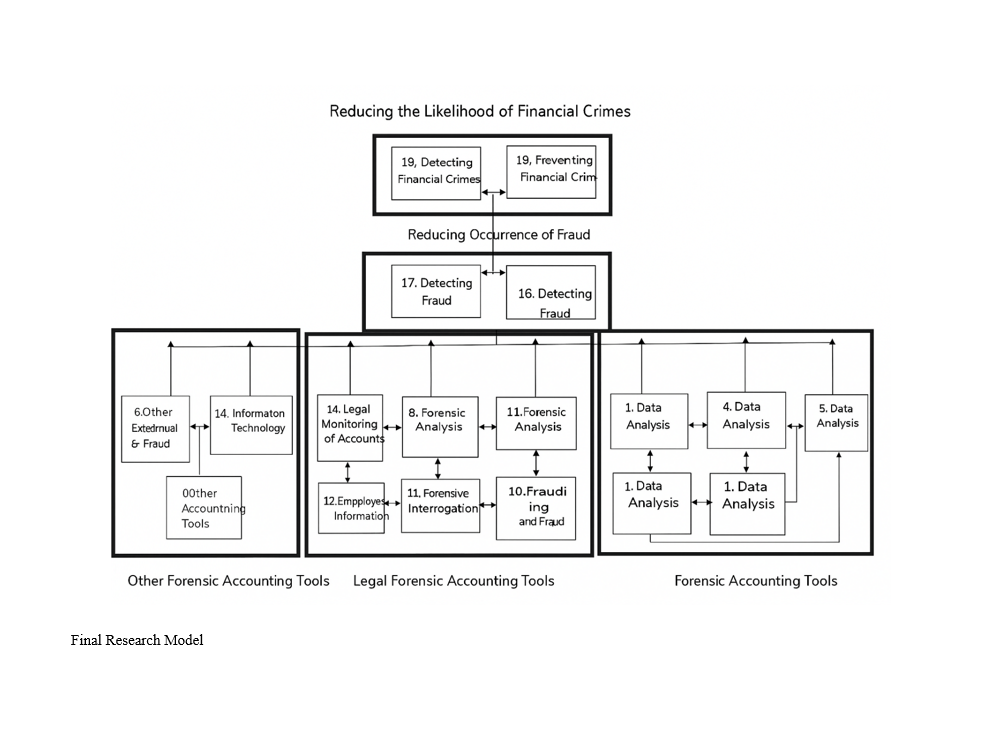

This study aims to propose a model for detecting the likelihood of fraud and financial crimes using forensic accounting tools. The required data were collected through semi-structured interviews with 15 expert forensic accountants using the snowball sampling method. An Interpretive Structural Modeling (ISM) approach was employed to develop a proposed model. According to the ISM analysis, the exploratory model includes 19 factors. The results revealed that forensic accounting tools include the following components: data analysis, accounting standards, auditing standards, financial ratio analysis, Benford's analysis, and cloud-based tools. Legal forensic accounting tools comprised components such as criminal and penal law, criminology, legal monitoring of individuals’ accounts, interviewing and interrogation, forensic analysis, and legal documentation. Other forensic accounting tools encompassed information technology, employee monitoring tools, and fraud psychology. Ultimately, accounting tools, legal tools, and other forensic accounting instruments contribute to reducing the incidence of fraud and financial crimes. This model provides a systematic framework for combating financial fraud by creating overlap among accounting, legal, and technological domains. The findings emphasize that integrating analytical tools (e.g., Benford's analysis) with advanced technologies (such as cloud systems) and legal mechanisms significantly enhances the accuracy and speed of fraud detection. Additionally, considering psychological and monitoring factors alongside legal requirements facilitates the design of more effective preventive policies. This model can serve as a foundation for developing forensic accounting standards and strengthening regulatory frameworks within organizations.

References

A. T. Tapang and J. U. Ihendinihu, "Effect of Forensic Accounting Services on Unethical Practices in Nigerian Banking Industry," The Journal of Accounting and Management; ZagrebVL - 10, no. 1, pp. 69-78, 2020.

O. E. Akinbowale, P. Mashigo, and M. F. Zerihun, "The integration of forensic accounting and big data technology frameworks for internal fraud mitigation in the banking industry," Cogent Business & Management, vol. 10, no. 1, 2023, doi: 10.1080/23311975.2022.2163560.

F. Hashem, "The Role of Forensic Accounting Techniques in Reducing Cloud Based Accounting Risks in the Jordanian Five Stars Hotels," WSEAS Transactions on Business and Economics, vol. 18, pp. 434-443, 2021, doi: 10.37394/23207.2021.18.44.

C. H. Yang and K. C. Lee, "Developing a strategy map for forensic accounting with fraud risk management: An integrated balanced scorecard-based decision model," Evaluation and program planning, vol. 80, p. 101780, 2020, doi: 10.1016/j.evalprogplan.2020.101780.

P. K. Ozili, Forensic accounting theory. Emerald Publishing Limited, 2020.

Ö. Arslan, The Forensic Accounting Profession and the Process of Its Development in the World. 2020, pp. 203-218.

M. Öztürk and H. Usul, Detection of Accounting Frauds Using the Rule-Based Expert Systems within the Scope of Forensic Accounting. 2020, pp. 155-171.

M. H. Ghaemi, M. Shahsavand, and A. Mohbi, "Explaining Forensic Accounting and Auditing Techniques and Their Application in Bankruptcy Detection," Professional Auditing Research Journal, vol. 2, no. 7, pp. 80-104, 2022.

S. F. Masoumi and M. Hekmati, "Organizational Transparency for Preventing Administrative and Financial Corruption (Case Study: Hamadan Municipality)," New Research Approaches in Management and Accounting Sciences, vol. 8, no. 28, pp. 2383-2397, 2024.

S. Chapushi-Shaqaqi, P. Khodabakhshi, and Honarmandi, "Identifying and Evaluating the Weaknesses of the Inspection and Audit System in Preventing Administrative and Financial Corruption in Sports Federations and Committees in Iran," Economic, Financial, and Accounting Studies Quarterly, vol. 42, no. 10, pp. 274-301, 2024.

A. Qahraman Nejad, "Reducing Administrative Corruption through Financial Oversight and Transparency in Municipalities towards Achieving Administrative Integrity in These Organizations," New Research Approaches in Management Sciences, vol. 37, no. 6, pp. 355-367, 2023.

A. Aminian and A. Tahriri, "Presenting a forensic accounting quality model in Iran based on interpretive structural modeling (ISM)," Journal of Accounting and Auditing Management Knowledge, vol. 11, no. 43, pp. 253-274, 2022.

A. Aminian and A. Tahriri, "Presenting an Interpretive Structural Model of Factors Affecting the Forensic Accounting Quality in Iran," International Journal of Finance & Managerial Accounting, vol. 7, no. 25, pp. 81-100, 2022.

H. Majboori Yazdi, S. A. Khalifeh Soltani, and R. Hejazi, "Developing a Fraud Detection Model in Forensic Accounting," Biannual Journal of Governmental Accounting, vol. 9, no. 18, pp. 1-32, 2023.

N. Dadashi and M. R. Pourali, "The Impact of Risk on Performance Considering Financial Constraints of Companies," Journal of Investment Knowledge, vol. 12, no. 47, pp. 217-230, 2023.

G. E. Oyedokun, "Determinants of Forensic Accounting Techniques and Theories: An Empirical Investigation," Annals of Spiru Haret University. Economic Series, vol. 22, no. 3, 2022, doi: 10.26458/22319.

L. H. Mahmood, "Detection of Corporate Fraud and Financial Distress: An Empirical Study Using Forensic Accounting Tools," THE COST AND MANAGEMENT, vol. 49, no. 3, pp. 60-67, 2021.

A. C. E. Amirian, M. H. Gholizadeh, and S. M. Mirbargkar, "Financial Crimes: Designing and Explaining a Model Using Grounded Theory," Scientific-Research Quarterly Journal of Investment Knowledge, vol. 10, no. 38, pp. 265-285, 2021.

D. A. Kulmie, M. D. Hilif, and M. Sheikh Hussein, "Socioeconomic Consequences of Corruption and Financial Crimes," International Journal of Economics and Financial Issues, vol. 13, no. 5, pp. 88-95, 2023, doi: 10.32479/ijefi.14714.

M. Yusuf and K. Harefa, "Forensic Accounting and Compliance Audit to Reduce the Number of Financial Fraud in Local Government," in 2nd International Conference of Strategic Issues on Economics, Business and, Education (ICoSIEBE 2021), 2022: Atlantis Press, pp. 18-29.

M. R. Pourali and F. Azareh, "Structural Model of the Impact of Dark Personality Traits on Audit Warning with the Mediating Role of Organizational Citizenship Behavior," Journal of Accounting and Auditing Research, vol. 15, no. 60SP - 43, p. 64, 2023.

M. Rad, "Proposing a Model for Predicting Fraud Probability in Financial Statements," 2022.

Downloads

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2025 Mohammad Reza Rahbari Karim Tehrani (Author); Mohammad Reza Pourali (Corresponding author); Mahmoud Samadi Largani (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.