Developing a Comprehensive Model of Psychological Factors Affecting Audit Quality in the Iranian Auditors' Community Based on the Grounded Theory Approach

Keywords:

Psychological factors, Audit quality, Grounded theory approach, auditors' communityAbstract

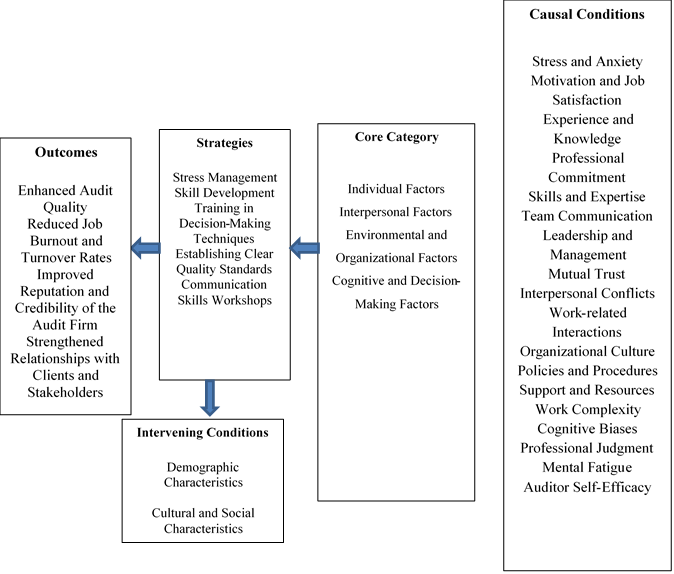

The purpose of this study is to develop a comprehensive model of psychological factors affecting audit quality in the Iranian auditors' community based on the grounded theory approach. The research is fundamental in terms of its objective and exploratory in nature. For data collection, a semi-structured in-depth interview approach was considered alongside library studies. This study, utilizing a qualitative approach and grounded theory methodology, aims to develop a comprehensive model of psychological factors influencing audit quality in the auditors' community. The statistical population of this research consisted of experts, specialists, and university professors in the field of auditing. Purposeful and snowball sampling methods were used to identify experts, and interviews were conducted with 10 experts based on data saturation. In the next step, 71 initial conceptual propositions were derived from open coding, 26 categorical propositions from axial coding, and 4 main categories from selective coding. According to the research findings, based on qualitative data, the psychological factors influencing audit quality can be categorized into four main groups: individual factors, interpersonal factors, environmental and organizational factors, and cognitive and decision-making factors. The study demonstrated that the impact of these factors on audit quality is both direct and indirect, and their interaction can either enhance or diminish audit quality. Identifying, understanding, and properly managing these factors help organizations and auditors improve their performance and enhance audit quality.

References

J. Sampet, N. Sarapaivanich, and P. G. Patterson, "The role of client participation and psychological comfort in driving perceptions of audit quality: evidence from an emerging economy," Asian Review of Accounting, vol. 27, no. 1, pp. 177-195, 2019, doi: 10.1108/ARA-09-2017-0144.

A. YaghobNejad, L. M. Samadi, and M. Poorali, "Evaluating the Effect of Auditors' Individual Psychological Bias and Personality Dimensions on Audit Quality," 2022. [Online]. Available: https://www.sid.ir/paper/416256/en.

H. N. Van, P. T. Hai, C. N. Thanh, D. N. Ngoc, and G. H. Hai, "Study on Factors Affecting Audit Fees and Audit Quality Through Auditors’ Perceptions: Evidence From an Emerging Economy," Problems and Perspectives in Management, vol. 20, no. 2, pp. 471-485, 2022, doi: 10.21511/ppm.20(2).2022.39.

N. A. Noordin, K. Hussainey, and A. F. Hayek, "The use of artificial intelligence and audit quality: An analysis from the perspectives of external auditors in the UAE," Journal of Risk and Financial Management, vol. 15, no. 8, p. 339, 2022, doi: 10.3390/jrfm15080339.

L. Chu, H. Fogel-Yaari, and P. Zhang, "The Estimated Propensity to Issue Going Concern Audit Reports and Audit Quality," Journal of Accounting, Auditing & Finance, vol. 39, no. 2, 2024, doi: 10.1177/0148558X221079011.

Y. Zheng, "Quality Management System and Audit Quality: The Moderating Effect of Independent Audit Inspection in China," Asian Journal of Accounting Perspectives, vol. 16, no. 1, pp. 26-53, 2023, doi: 10.22452/ajap.vol16no1.2.

L. Y. Lee and A. Mohammed Isa, "Client narcissism and audit quality: The moderating role of auditors' self-esteem," Accounting Review, 2022.

M. Athavale, Z. Guo, Y. Meng, and T. Zhang, "Diversity of signing auditors and audit quality: Evidence from capital market in China," International Review of Economics & Finance, vol. 78, pp. 554-571, 2022/03/01/ 2022. [Online]. Available: https://doi.org/10.1016/j.iref.2021.12.020.

N. Shahmoradi and Z. Tabatabaienasab, "The effect of Audit Quality on the Relationship between Economic Uncertainty and Accrual Based Earnings Management in Listed Companies in Tehran Stock Exchange," Financial Accounting Research, vol. 13, no. 1, pp. 67-86, 2021. [Online]. Available: https://far.ui.ac.ir/article_25426_en.html?lang=en.

C. M. Nwoye, A. S. Anichebe, and I. F. Osegbue, "Effect of audit quality on earnings management in insurance companies in Nigeria," Athens Journal of Business & Economics, vol. 7, no. 2, pp. 173-202, 2021, doi: 10.30958/ajbe.7-2-4.

D. Tania, M. Tarmizi, and M. Adrian, "Determinants of Audit Quality in Companies That Conduct Initial Public Offerings," Journal of Accounting Science, vol. 7, no. 1, pp. 54-62, 2023, doi: 10.21070/jas.v7i1.1666.

M. Shabani, "The Moderating Role of Audit Quality on the Impact of Internal Control Significance on Cash Flow Risk," in 12th International Conference on Accounting, Management, and Innovation in Business, Tehran, 2023. [Online]. Available: https://civilica.com/doc/1720075/.

K. R. Salman and B. Setyaningrum, "The Effects of Audit Firm Size, Audit Tenure, and Audit Rotation on Audit Quality," Ilomata International Journal of Tax and Accounting, vol. 4, no. 1, pp. 92-103, 2023, doi: 10.52728/ijtc.v4i1.636.

I. Illahi, N. Sumarni, and Z. Maiza, "Transfer Pricing and Tax Avoidance: Moderating Role of Audit Quality," Jifa (Journal of Islamic Finance and Accounting), vol. 5, no. 2, pp. 89-97, 2023, doi: 10.22515/jifa.v5i2.6537.

M. Delbari Raghb and A. Ismailzadeh Moghri, "Independent Audit Quality Model Emphasizing Stakeholder Needs," Financial Accounting and Auditing Research, vol. 15, no. 1, pp. 69-98, 2023. [Online]. Available: https://acctgrev.ut.ac.ir/article_88664.html.

W. Anding, M. J. Mowchan, T. A. Seidel, and A. Zimmerman, "Audit Partners in Leadership Roles: Implications for Audit Quality," Available at SSRN 3694031, 2023. [Online]. Available: https://doi.org/10.2139/ssrn.3694031.

Y. Yulianti, M. W. Zarkasyi, H. Suharman, and R. Soemantri, "Effects of professional commitment, commitment to ethics, internal locus of control and emotional intelligence on the ability to detect fraud through reduced audit quality behaviors," Journal of Islamic Accounting and Business Research, 2023, doi: 10.1108/JIABR-02-2021-0076.

V. M. Pattiasina, Y. Noch, H. Surijadi, M. Amin, and E. Y. Tamaela, "The relationship of auditor competence and independence on audit quality: An assessment of auditor ethics moderation and professional commitment," Indonesia Accounting Journal, pp. 14-26, 2021, doi: 10.32400/iaj.31289.

M. Bani, K. Faghani Makrani, and A. Zabihi, "The Impact of Professional Commitment and Ethical Ideology on Audit Quality by Mediating the Ethical Behavior of Governmental Firms Auditors in Structural Equation Modeling," Governmental Accounting, vol. 6, no. 1, pp. 81-96, 2020. [Online]. Available: https://gaa.journals.pnu.ac.ir/article_7161.html?lang=en.

A. Daryaei and A. Azizi, "The Relationship Between Ethics, Experience, and Professional Competence of Auditors with Audit Quality (Considering the Moderating Role of Professional Skepticism)," Journal of Financial Accounting Knowledge, vol. 5, no. 1, pp. 79-99, 2018.

S. T., "Relationship between Auditor Professional Ethics and Audit Quality," (in eng), Ethics in Science and Technology, Research vol. 11, no. 3, pp. 77-86, 2017. [Online]. Available: http://ethicsjournal.ir/article-1-374-en.html.

T.-K. Chou, J. A. Pittman, and Z. Zhuang, "The Importance of Partner Narcissism to Audit Quality: Evidence from Taiwan," The Accounting Review, vol. 96, no. 6, pp. 103-127, 2021, doi: 10.2308/tar-2018-0420.

K. F. Aswar, M. Givari Akbar, E. Wiguna, and E. Hariyani, "Determinants of Audit Quality: Role of Time Budget Pressure," Problems and Perspectives in Management, vol. 19, no. 2, pp. 308-319, 2021, doi: 10.21511/ppm.19(2).2021.25.

M. Ettredge, L. Fuerherm, and C. Li, "Fee Pressure and Audit Quality," Accounting, Organizations and Society, vol. 39, no. 4, pp. 182-214, 2013, doi: 10.1016/j.aos.2014.04.002.

T. D. Bauer, "Fatigue impairment in auditing: Evidence from archival and experimental studies," Accounting, Organizations and Society V1 - 101167, 2019.

C. Liu, "The impact of emotional intelligence on auditors' skepticism and decision-making quality," Contemporary Accounting Research, vol. 37, no. 1, pp. 395-421, 2020.

E. Aschauer, M. Fink, A. Moro, K. Van Bakel-Auer, and B. Warming-Rasmussen, "Trust and professional skepticism in the relationship between auditors and clients: overcoming the dichotomy," Behavioral Research in Accounting, vol. 29, no. 1, pp. 19-42, 2017, doi: 10.2308/bria-51654.

D. Maresch, E. Aschauer, and M. Fink, "Competence trust, goodwill trust and negotiation power in auditor-client relationships," Accounting, Auditing and Accountability Journal, vol. 33, no. 2, pp. 335-355, 2020, doi: 10.1108/AAAJ-02-2017-2865.

N. A. Rahman, Z. Yaacob, and R. M. Radzi, "The challenges among Malaysian SME: a theoretical perspective," World Journal of Social Sciences, vol. 6, no. 3, pp. 124-132, 2016.

S. Buchheit, D. W. Dalton, N. L. Harp, and C. W. Hollingsworth, "Auditors' bias and sub-conscious processing: Implications for audit quality," Accounting, Organizations and Society, vol. 51, pp. 167-183, 2019.

I. Ayemere, "The effects of time pressure and conscientiousness on internal auditors' performance," Auditing: A Journal of Practice & Theory, vol. 37, no. 4, pp. 127-144, 2023.

T. Jones and S. F. Taylor, "Service loyalty: accounting for social capital," Journal of Services Marketing, vol. 26, no. 1, pp. 60-74, 2021, doi: 10.1108/08876041211199733.

J. C. Sweeney, A. Payne, P. Frow, and D. Liu, "Customer advocacy: a distinctive form of word of mouth," Journal of Service Research, vol. 23, no. 1, pp. 139-155, 2020, doi: 10.1177/1094670519900541.

A. Wieland, F. Kock, and A. Josiassen, "Scale purification: state-of-the-art review and guidelines," International Journal of Contemporary Hospitality Management, vol. 33, no. 11, pp. 3346-3362, 2018, doi: 10.1108/IJCHM-11-2017-0740.

N. Rezaei, B. Bani Mahd, and S. H. Hosseini, "The Impact of Organizational and Professional Identity on the Professional Skepticism of Independent Auditors," Audit Knowledge Quarterly, vol. 18, no. 71, pp. 175-199, 2018.

K. W. Chan, C. K. Yim, and S. Lam, "Is customer participation in value creation a double edged sword? Evidence from professional financial services across cultures," Journal of Marketing, vol. 74, no. 3, pp. 48-64, 2020, doi: 10.1509/jmkg.74.3.048.

Additional Files

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2025 Management Strategies and Engineering Sciences

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.