Exploring Human Resource Auditing Components for Performance Evaluation

Keywords:

metacombination, performance, Human resources auditAbstract

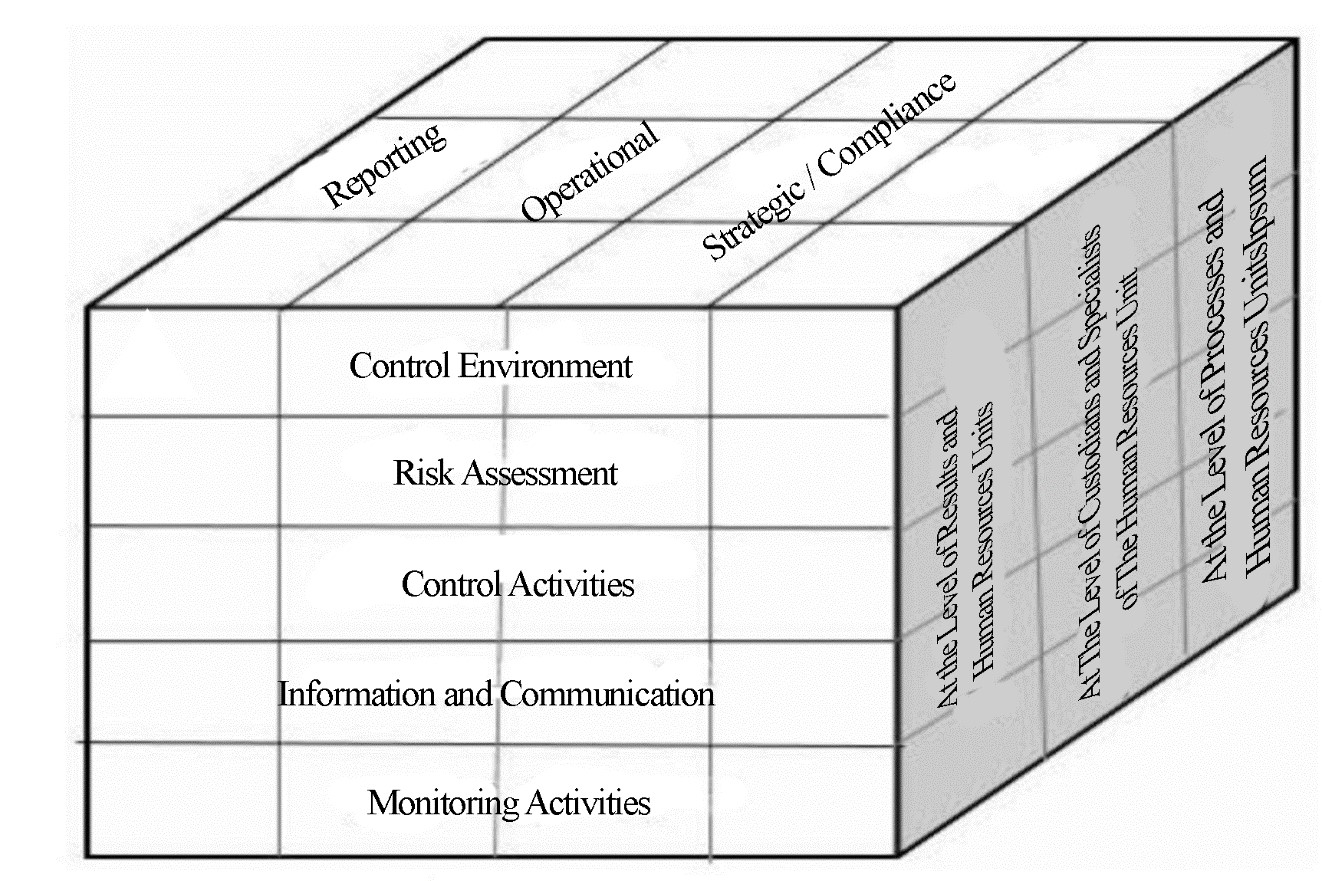

The internal auditing profession in Iran is currently going through a genuine maturation phase, marked by the pivotal release of the internal control guidelines published by the Securities and Exchange Organization. A significant portion of the cultural groundwork is still in its initial stages, and the understanding of internal auditing, along with the expectations of managers regarding internal audits, has been effectively clarified and explained. In this context, the present study delves into the components of human resource auditing in relation to performance evaluation. The research utilizes an exploratory mixed-methods design. In the first phase, qualitative methods were employed to uncover constructs and causal mechanisms between them, while in the subsequent phase, quantitative methods were applied to a larger sample to confirm the relationships between the constructs and achieve an acceptable level of generalizability. After categorizing the extracted codes, the researcher used open coding to summarize the homogeneous data, and the codes were classified into concepts and categories based on conceptual similarity, frequency, and significance, focusing on the objectives and levels of human resource auditing. The results revealed that the process and activity level of the human resources unit includes the evaluation of all defined processes within the human resources unit, such as developmental processes and administrative matters. This level, as identified in various studies, has been labeled under different codes like internal aspects of processes, functional level, internal environment of the unit, developmental processes level, lower level, and technical level, with all these descriptions pointing to a common underlying concept. Overall, in comparison to the general framework, three entirely new levels were identified: the human resources unit's results level, the level of custodians and specialists in the human resources unit, and the process and activity level of the human resources unit. These were recognized as subcategories for auditing at the operational level, which is one of the levels of the general framework, and were identified for human resource auditing.